What is FIRE (the 4% rule)

FIRE stands for Financial Independence Retire Early.

It was a movement where workers aim to retire early ASAP.

Instead of working up to 60 to 70 years where you don’t have the health and energy anymore once you retire, FIRE instead aims to retire as early as possible. Some have done it in just 10 years of working or some before turning 40 years old.

To Retire Early, you need to:

First, save a lot of money

Then, invest that savings

The FIRE promise is that by doing these 2-steps aggressively, you can achieve early retirement.

But how early?

The FIRE movement was based on study called the Trinity Study.

The Trinity Study goal is to determine how much is the Safe Withdrawal Rate % (SWR).

The SWR is the amount you can withdraw from your retirement yearly and never run out of money.

How is that possible?

It assumes that your retirement money will earn returns to offset your withdrawals.

The study assumes a 60/40 portfolio (60% stocks and 40% bonds)

The study concludes that the safe withdrawal rate or the amount you can withdraw annually from your portfolio is 4%.

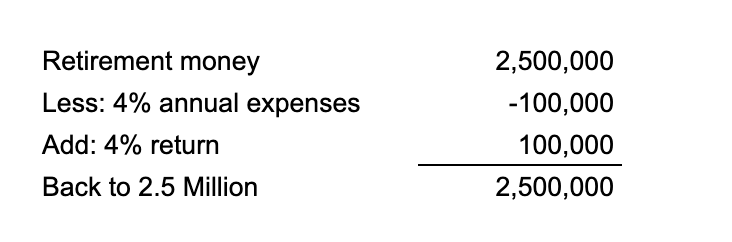

So, from that you can work back how much you need to retire, which would 25x your annual expenses.

Why 25x? because if you have 100,000 living expenses per year, the amount you need to retire is 2,500,000 (100,000 multiply by 25)

4% of 2,500,000 is the amount you will need to withdraw which is 100,000 which is also equivalent to your annual living expense

The assumption is that your 2,500,000 retirement money will also earn 4%:

The idea is to live on the return earned by your retirement savings.

If you want to read more about this study, here is a great article explaining it in more detail: Updated Trinity Study and the 4% Rule - 2024 and Beyond

Is FIRE really possible?

Studies like this should only be used as a guide. Not a goalpost.

What I meant is that don’t try to get obsessed with hitting your 25x of your annual living expenses.

Also, if you blindly follow this study, you will assume that the returns of the past will be replicated in the future.

The study assumes heavy allocation into index funds like S&P500 ETFs.

However, those funds are not easily accessible here in the Philippines.

If you happen to have access to those, you assumed that the returns of the index S&P500 will be replicated in the future.

Where you invest your money is a personal thing that only you can determine.

Like I said in some of my blog, I was into the FIRE movement when I started working.

But since I didn’t had access to S&P500 funds in 20171

I was left with no choice but to go with Philippine Stock Exchange Index (PSEi) funds. From 2017 to 2022 I got demotivated saving and investing because my PSEi mutual funds went nowhere.

In 2022, I discovered bitcoin, my FIRE dreams started to be revived again. But the difference is that I am not focus on that day anymore when I will hit my 25x of my living expenses.

If you focus on the end goal of when that happens, you will miss your daily life. I’m trying just to live in the moment.

It doesn’t mean that I won’t save aggressively. I am still saving aggressively to the point that I took on debts to invest in an asset (not Index funds) that I believe will grow my savings over time. I talk more about that here in this post.

Life circumstances also can change, your expenses will change in the future. You will perhaps buy a house or car, get married have children etc.

If you focus too much on a fixed goal in the future, you may miss out on living your life now. And look, I am not saying to YOLO your salary & savings into things you don’t need to impress people you don’t even like.

Saving as much as possible is still the best thing you can do, especially in today’s world when it is harder to save money because of two things:

Inflation or the debasement of money - Your 100,000 now will not be the same in the next year, 5 years or 10 years. Taxes and death are not the only 2 things for certain. Inflation is also a sure thing now. Your money will definitely buy less in the future.

High time preference environment/culture - What this simply means is that we live in a YOLO (You Only Live Once) mentality. We live in a have fun now forget about the future mentality. Just take a look at our everyday lives. We eat pleasurable foods and don’t think about our health. We live on screens trying to find pleasurable things to watch, play, do etc. We don’t read books anymore. If you have read this far on this blog. I admire you.

Partying, drinking, drugs, gambling, affairs are the normal anymore. You can probably name people in your life who’s either a gambler, alcoholic, drug addict or is having an affair. Our culture today encourages having fun now instead of saving for our future.

To help in your FIRE journey, you need an antidote to these two things (inflation & high-time preference) that make savings harder. You need to save your money into something that is the opposite of Inflationary and High-time preference.

That thing is bitcoin. Bitcoin was created to be anti-inflation or anti-debasement money despite the volatility because of the limit on its supply.

Bitcoin is limited to 21,000,000 only unlike the dollar or any other currency which is printed to infinity, which happens to be the reason why we have inflation.

By having a money that you can truly save because it is not printed to infinity, it will motivate you to have a low-time preference or to delay gratification.

Instead of having fun now or throwing your money away, you will be less likely to do that because you have money that you can save.

Most people think that investing in bitcoin is only about making money, but if you truly believe in bitcoin, you know it is savings.

The gains/returns in every investment is actually partly a reflection of inflation or debasement.

It is not just goods and services that inflate, assets inflate in value also. Thats why investing has become savings. Because your cash won’t grow to keep up inflation. You can’t save money in food even though it inflates, because your food will rot.

S&P 500 has kept track with the growth in money supply (the total amount of money printed).

Before bitcoin, S&P 500 was probably the best thing. But now we have bitcoin, I believe it is the best savings tool for the foreseeable future.

How bitcoin can help you FIRE

Even though generally I don’t like FIRE people maximalist because they think that the 4% rule is a gospel, I still admire their perseverance. I admire their choice with life of saving for the future rather than living a YOLO materialistic life.

But what I’m saying to FIRE people is also to look into bitcoin.

Personally, I am not confident to put 100% of my savings into index funds.

Because I believe that bitcoin is the fastest horse in the race.

I’m not saying to sell all your index funds to buy bitcoin. I suggest (Not Financial Advice) to take a look at bitcoin with an open mind, perhaps buy 1%, if you own it, you will probably be motivated to learn more about it.

Only you can determine where to put your FIRE money.

But what I can say is that S&P500 has become a crowded long-term trade, it’s like a ship full of people where there’s no more room for more people. Not saying it won’t go up anymore, it will definitely go up because more money will be printed.

With bitcoin, we are still early, there’s a lot of room to grow.

That’s why most people like FIRE people don’t invest in it. That’s how you 100x. When you get in early when most people are ignoring it.

I believe some banks like Security Bank offered feeder funds that invests in S&P500 funds at that time, but the minimum is 50,000. I was earning 20,000 a month at that time.

where or what app do you buy bitcoin?